March 25th, 2022

Posted in:

Related Articles

April 25th, 2024

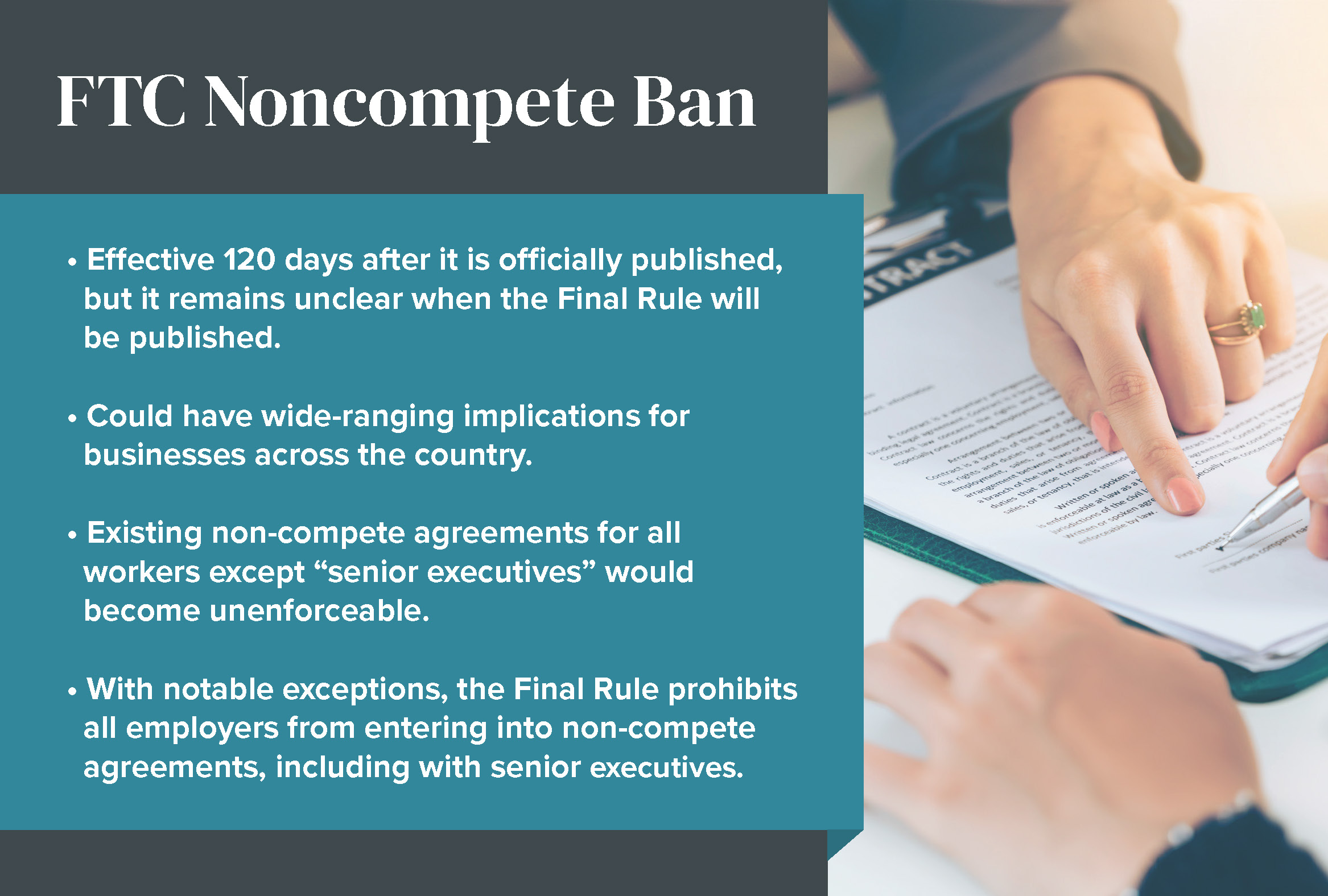

FTC Issues Ban on Noncompete Agreements

On April 23, 2024, the Federal Trade Commission (FTC) announced a Final Rule, applicable to for-profit employers, that would prohibit the enforcement of most “noncompete” clauses—those clauses that prohibit “workers” from seeking or accepting competing…

April 15th, 2024

To Be Blunt: The Dormant Commerce Clause Held To Not Apply to Maryland’s Social Equity Cannabis Licensing Scheme

The below information is provided as an update on an important issue developing with respect to Maryland’s cannabis industry. However, if you are interested in starting a cannabis-related business or providing ancillary services to a…